When Will Mortgage Rates Ease?

Homebuying Tips

Homebuying Tips

One of the most pressing questions in today’s real estate market is: When will mortgage rates finally come down? After several years of steadily rising rates and a volatile 2024, many homebuyers, sellers, and real estate professionals are eagerly awaiting a shift toward more favorable conditions.

While predicting the future of mortgage rates with complete certainty is impossible, leading experts and recent forecasts offer some clarity about what we might expect in 2025. Here’s an overview of the current projections and factors that could shape the mortgage rate landscape moving forward.

After significant fluctuations in 2024, the latest forecasts suggest mortgage rates will stabilize and gradually ease over the coming year. According to data from Fannie Mae, the Mortgage Bankers Association (MBA), and Wells Fargo, the average rate for a 30-year fixed mortgage could drop to 6.33% by the end of 2025. For perspective, here’s how the quarterly projections break down:

| Quarter | Fannie Mae | MBA | Wells Fargo | Average of All Three |

|---|---|---|---|---|

| 2024 Q4 | 6.60% | 6.60% | 6.80% | 6.67% |

| 2025 Q1 | 6.50% | 6.60% | 6.65% | 6.58% |

| 2025 Q2 | 6.40% | 6.50% | 6.45% | 6.45% |

| 2025 Q3 | 6.30% | 6.40% | 6.25% | 6.32% |

| 2025 Q4 | 6.30% | 6.40% | 6.30% | 6.33% |

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“While mortgage rates remain elevated, they are expected to stabilize.”

This expected stabilization brings some optimism to a market that’s been navigating a challenging rate environment.

It’s essential to understand that the trajectory of mortgage rates depends on several dynamic economic variables. Here are three key factors to watch:

Inflation Trends

The Federal Reserve’s primary focus is combating inflation. If inflation continues to cool, rates could drop further. Conversely, persistently high inflation may keep rates elevated for a longer period.

Unemployment and Economic Growth

The labor market plays a critical role in the Fed’s monetary policy decisions. Lower unemployment rates typically indicate economic strength but can also influence the Fed’s stance on rate adjustments.

Government Policies

With a new administration set to take office in January, upcoming fiscal and monetary policies could shape how financial markets respond. Any significant policy shifts may directly impact investor confidence and mortgage rates.

As economic conditions evolve, these forecasts are subject to change. That’s why it’s crucial to stay informed and work with experienced professionals who can help you navigate the market.

Instead of trying to “time the market,” focus on the factors within your control:

By preparing proactively, you’ll be well-positioned to take advantage of any opportunities that arise when rates begin to decline.

While mortgage rates are expected to ease in 2025, the path forward will be influenced by various economic factors. If you’re planning to buy or sell a home, let’s connect to ensure you have the most up-to-date information and expert guidance to achieve your goals in today’s ever-changing market.

Stay up to date on the latest real estate trends.

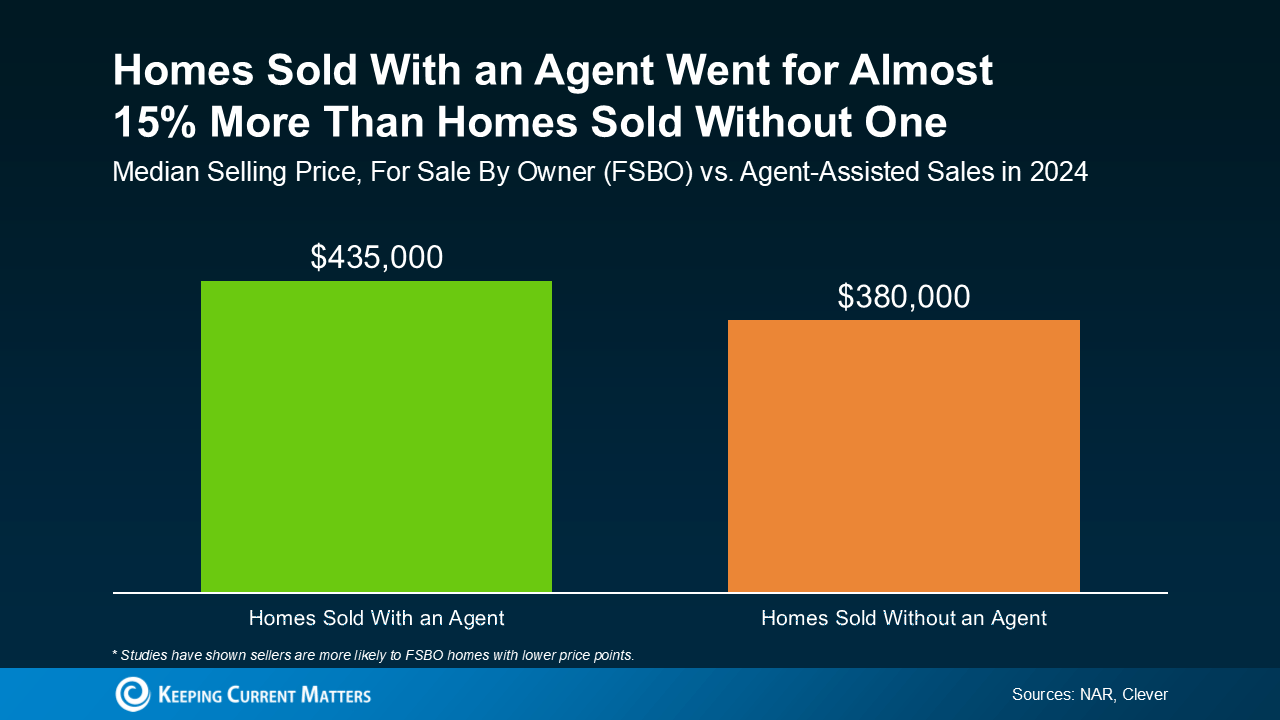

Why FSBO Sellers Often Lose Money in Today’s Market

Why First-Time Buyers in San Marcos May Finally Catch a Break in Today’s Market

How To Sell Real Estate

In today’s market, first impressions happen at lightning speed—and most buyers make snap judgments based on photos alone.

A Pilot Project That Didn’t Pan Out

The Waymaker Advantage: Personal, Purpose-Driven Service

You’ve Built Equity. Now It Might Be Time To Share It.

Homebuying Tips

Buying a Home? Start with the Basics

How Attending Open Houses—and Working with Waymaker Realty Advisors—Gives California Buyers a Clear Advantage

How a Well-Executed Open House Can Spark Bidding Wars, Showcase Lifestyle, and Sell Faster in San Marcos

You’ve got questions and we can’t wait to answer them.