Consumer Guide: Fire Damage and Policy Coverage

San Diego

San Diego

The REALTORS® Relief Foundation is currently accepting donations to support victims of the devastating January 2025 California wildfires. To contribute, text RRFCAStrong to 71777 or visit rrf.realtor by January 31, 2025. Every dollar donated goes directly to wildfire victims.

Most homeowners insurance policies include coverage for fire and smoke damage, but coverage limitations can vary depending on your property's location and risk level. If you live in an area prone to wildfires, insurers may limit coverage or decline to offer a policy altogether. It is crucial to review your policy and consult an insurance agent to determine whether additional coverage is necessary. A REALTOR® can also help guide you in understanding your options.

In general, a standard homeowners insurance policy covers:

Structural damage to your home

Other structures on your property (such as detached garages or sheds)

Personal belongings damaged or destroyed by fire

This applies to fires caused by natural disasters, electrical malfunctions, and accidental incidents. However, insurance policies may not cover fire damage resulting from:

Nuclear hazards

Arson committed by the homeowner

Poor maintenance or neglect

Gradual wear and tear

For clarification on your specific policy, reach out to your insurance provider.

Some private insurance providers exclude fire damage coverage in high-risk areas, similar to flood insurance. If you are unable to secure coverage, consider:

Shopping around: Different insurers have different risk tolerances.

Exploring surplus lines insurance: These “non-admitted” insurers provide policies for high-risk properties, though they are regulated differently and do not participate in state insurance guaranty funds.

Contacting a surplus lines broker: Your state insurance department or current insurance agent can refer you to specialized brokers who cover high-risk properties.

If your home is deemed too high-risk by insurers, consider these steps to manage costs and secure coverage:

Consult with an insurance professional to explore your options.

Compare multiple quotes, including those from surplus lines brokers.

Obtain a wildfire-prepared certification from organizations like the Institute for Building & Home Safety.

Contact your state insurance commissioner for guidance on fire insurance options and risk maps.

If traditional insurance is unavailable, you may qualify for a Fair Access to Insurance Requirements (FAIR) Plan. These government-backed plans provide coverage for high-risk properties that cannot secure insurance on the private market. While typically more expensive and offering limited protections, a FAIR plan serves as a last-resort option for homeowners unable to obtain private insurance.

Fire damage policies and insurance regulations vary by state. Speak with your real estate professional or an attorney to understand your options in your specific location. For additional resources, visit facts.realtor.

By staying informed and proactive, homeowners can better protect their properties and ensure they have the necessary coverage in the event of a wildfire or fire-related disaster.

Stay up to date on the latest real estate trends.

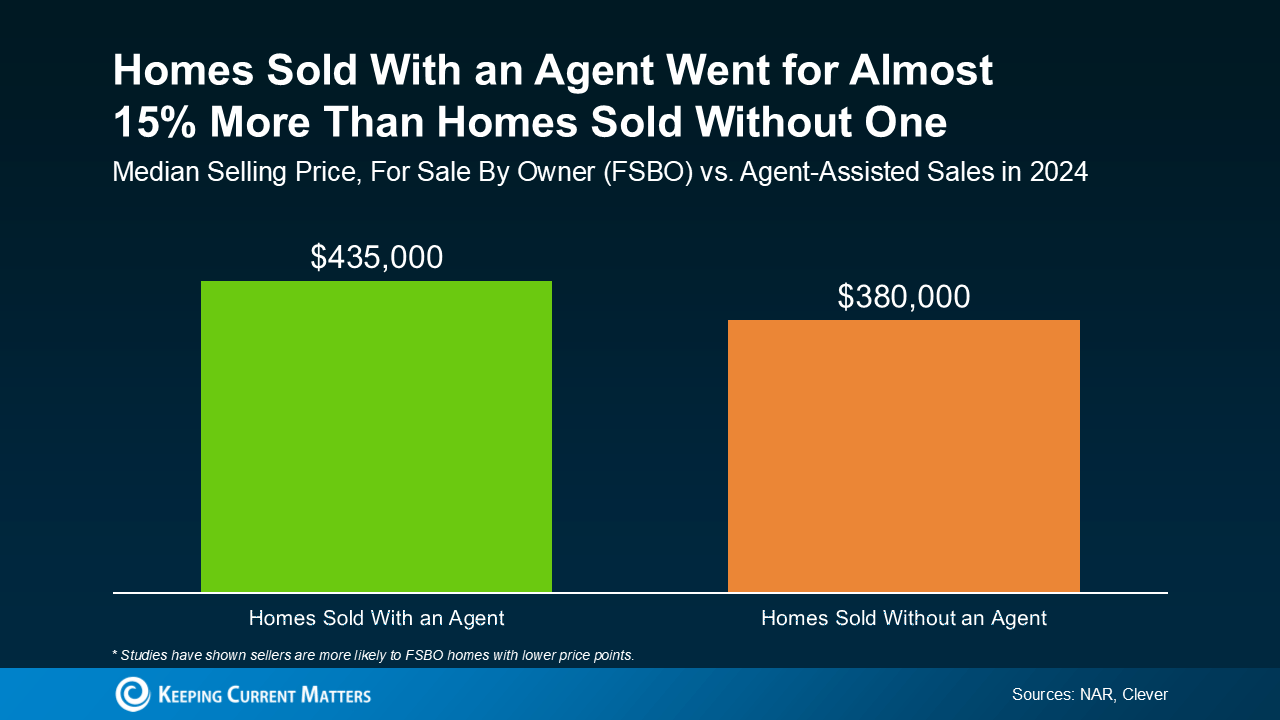

Why FSBO Sellers Often Lose Money in Today’s Market

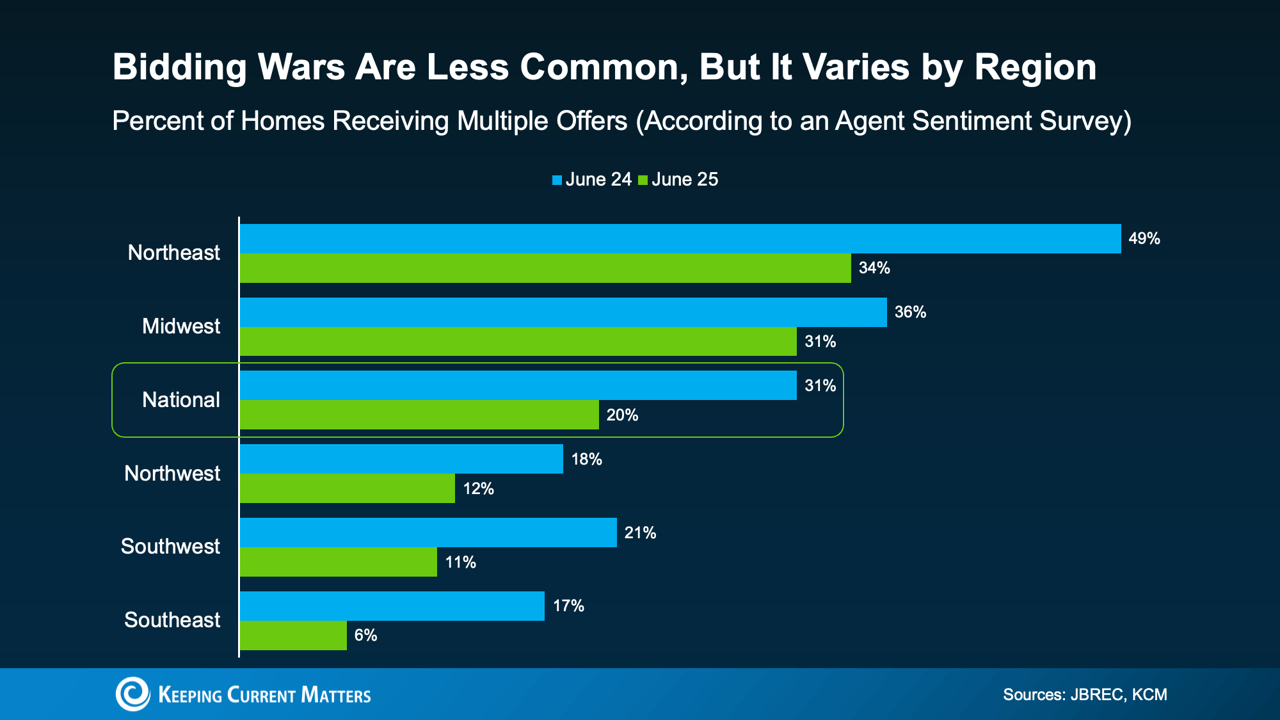

Why First-Time Buyers in San Marcos May Finally Catch a Break in Today’s Market

How To Sell Real Estate

In today’s market, first impressions happen at lightning speed—and most buyers make snap judgments based on photos alone.

A Pilot Project That Didn’t Pan Out

The Waymaker Advantage: Personal, Purpose-Driven Service

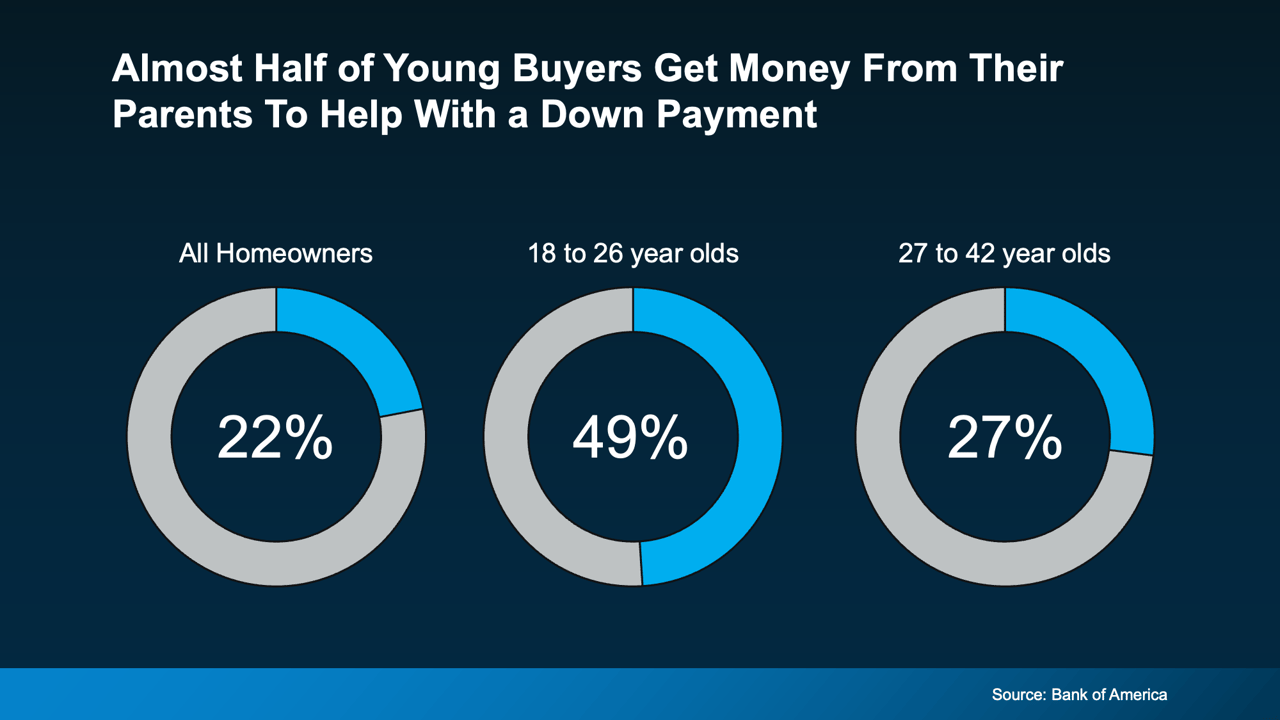

You’ve Built Equity. Now It Might Be Time To Share It.

Homebuying Tips

Buying a Home? Start with the Basics

How Attending Open Houses—and Working with Waymaker Realty Advisors—Gives California Buyers a Clear Advantage

How a Well-Executed Open House Can Spark Bidding Wars, Showcase Lifestyle, and Sell Faster in San Marcos

You’ve got questions and we can’t wait to answer them.